Personal Loan Meaning: Understanding and Utilizing Personal Loans

Explore the ins and outs of personal loans, covering interest rates. Expert tips to help you confidently achieve your financial goals navigate.

There are different types of Personal Loans

Personal loans come in various forms, including:

-

Fixed-Rate Loans: The interest rate remains constant throughout the loan term, making monthly payments predictable.

-

Variable-Rate Loans: The interest rate fluctuates based on market conditions, which may cause monthly payments to vary.

-

Secured Loans: These loans require collateral, such as a home or vehicle, which the lender can seize if the borrower defaults on the loan.

-

Unsecured Loans: These loans do not require collateral, making them riskier for lenders and often resulting in higher interest rates.

-

Co-Signed Loans: A co-signer with a good credit history can help a borrower with poor or limited credit history qualify for a loan and secure better loan terms.

Benefits of Personal Loans

Some of the advantages of personal loans include:

Flexibility: Personal loans can be used for various purposes, providing financial freedom and flexibility to borrowers.

Lower Interest Rates: Personal loans typically have lower interest rates compared to credit cards, making them a more cost-effective option for financing large expenses.

Fixed Repayment Terms: With fixed-rate personal loans, borrowers know exactly how much they need to pay each month and can easily budget for the loan repayment.

Debt Consolidation: Personal loans can be used to consolidate high-interest debt, such as credit card balances, into a single loan with a lower interest rate, simplifying debt management.

Go check out!!

- 5 Best Motor Insurance Policies To Buy in India

- How To Buy The Best Health Insurance In India

- What Is Mutual Funds: How To Invest In Mutual Funds

- Motor Insurance Policy: Benefits of Motor Insurance

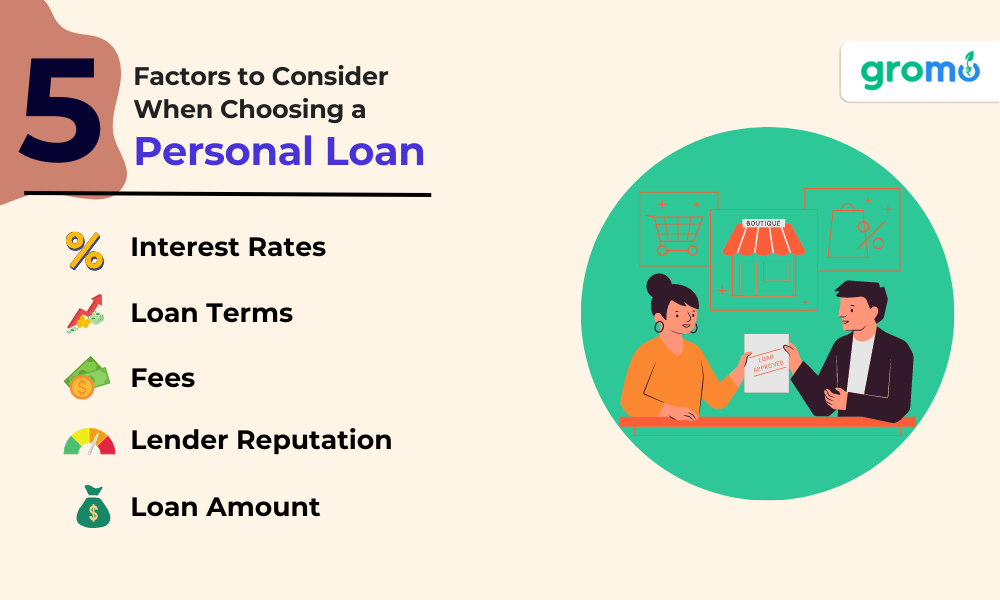

Factors to Consider When Choosing a Personal Loan

When selecting a personal loan, consider the following factors:

-

Interest Rates: Compare rates from multiple lenders to find the most competitive offer.

-

Loan Terms: Evaluate the loan term length, as shorter terms typically result in lower overall costs but higher monthly payments.

-

Fees: Be aware of origination fees, prepayment penalties, and late payment fees, as they can impact the total cost of the loan.

-

Lender Reputation: Research the lender's reputation, customer service, and transparency to ensure a positive borrowing experience.

-

Loan Amount: Ensure the loan amount meets your financial needs without borrowing excessively.

How to Apply for a Personal Loan

Follow these steps to apply for a personal loan:

Check Your Credit Score: A higher

Credit score increases the likelihood of loan approval and favorable loan terms.

Research Lenders: Compare loan offers from banks, credit unions, and online lenders to find the best fit for your needs.

-

Gather Necessary Documents: Prepare documents, such as proof of income, employment verification, and recent bank statements, to streamline the application process.

-

Submit an Application: Complete and submit the loan application, either online or in person, providing accurate and up-to-date information.

-

Review Loan Offers: If approved, carefully review the loan agreement, paying close attention to interest rates, fees, and repayment terms.

-

Accept the Loan Offer: If satisfied with the loan terms, sign the loan agreement and accept the loan offer.

-

Receive Funds: The lender will disburse the funds directly to your bank account or to the designated payee, such as a credit card company for debt consolidation.

Alternatives to Personal Loans

Consider these alternatives to personal loans:

-

Credit Cards: For smaller expenses or short-term borrowing, credit cards may offer a convenient alternative, especially if the cardholder can take advantage of an introductory 0% APR offer.

-

Home Equity Loans or Lines of Credit: Homeowners can use their home equity as collateral for a loan or line of credit, which typically results in lower interest rates compared to unsecured personal loans.

-

401(k) Loans: Borrowing from a 401(k) account may provide a low-interest option for short-term financial needs, but it can also impact retirement savings and have tax implications.

-

Peer-to-Peer Lending: P2P lending platforms connect borrowers with individual investors, often offering competitive interest rates.

Personal loans offer a flexible and convenient financing option for various needs and circumstances. By understanding the different types of personal loans, their benefits, and factors to consider when choosing a loan, borrowers can make informed decisions that support their financial goals.

Additionally, it's essential to explore alternatives to personal loans to determine the most suitable financing option for each individual's unique situation.

Tips for Managing Personal Loans

Once you've obtained a personal loan, follow these tips to manage it effectively and ensure timely repayment:

-

Create a Budget: Develop a monthly budget that accounts for the loan repayment, ensuring you allocate sufficient funds to cover the monthly payment.

-

Set Up Automatic Payments: Enroll in automatic payments to avoid missed or late payments, which can negatively impact your credit score and result in additional fees.

-

Pay Extra When Possible: If your budget allows, make extra payments or pay more than the minimum payment to reduce the loan balance and save on interest costs.

-

Monitor Your Credit: Regularly check your credit report to ensure the personal loan and payment history are accurately reported, and promptly address any discrepancies.

-

Stay in Contact with Your Lender: Keep your lender informed of any changes in your financial situation or contact information, and reach out to them if you're experiencing difficulty making payments to discuss potential solutions.

Personal Loan Scams: How to Identify and Avoid Them

Borrowers should be cautious of potential personal loan scams, which can result in financial loss and damaged credit. Here are some warning signs and tips for avoiding scams:

-

Upfront Fees: Legitimate lenders may charge origination fees, but they typically deduct these fees from the loan amount rather than requiring upfront payment.

-

Guaranteed Approval: No reputable lender can guarantee loan approval without first assessing the borrower's creditworthiness and financial situation.

-

Unsolicited Offers: Be cautious of unsolicited loan offers, especially if they're received via email, phone calls, or text messages from unknown sources.

-

Unprofessional Websites or Communications: Watch for poorly designed websites, spelling and grammar errors, or unprofessional communication, which may indicate a scam operation.

-

Verify Lender Credentials: Research the lender's licensing and registration information through official channels, such as the Better Business Bureau or state regulatory agencies.

By staying vigilant and conducting thorough research, borrowers can protect themselves from personal loan scams and make informed decisions when seeking legitimate loan options.

NOW! you can sell financial products online on GroMo install the app and earn your income sitting at home.

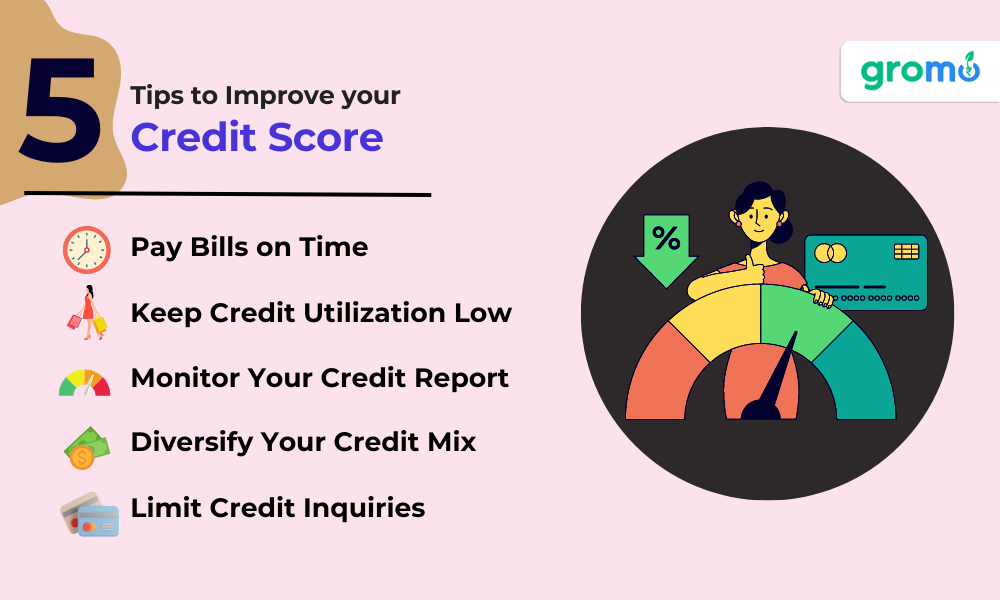

Improving Your Credit for Better Personal Loan Options

A strong credit score can help borrowers secure more favorable personal loan terms, such as lower interest rates and higher loan amounts.

Follow these tips to improve your credit:

Pay Bills on Time: Consistently paying bills on time is crucial for maintaining and improving your credit score.

Keep Credit Utilization Low: Aim to use no more than 30% of your available credit at any given time to avoid negatively impacting your credit score.

Monitor Your Credit Report: Regularly review your credit report for errors or inaccuracies and dispute any incorrect information.

Diversify Your Credit Mix: Maintain a mix of different credit types, such as credit cards, installment loans, and mortgages, to demonstrate responsible credit management.

Limit Credit Inquiries: Avoid applying for multiple credit accounts within a short period, as this can temporarily lower your credit score.

By implementing these strategies, borrowers can improve their credit scores over time and increase their chances of securing favorable personal loan terms.

Debt Consolidation vs. Debt Settlement: Understanding the Differences

When managing debt, borrowers may consider debt consolidation or debt settlement as potential solutions. It's essential to understand the differences between these approaches:

Debt Consolidation

Debt consolidation involves combining multiple high-interest debts, such as credit card balances, into a single loan with a lower interest rate. This simplifies debt management and can reduce overall interest costs. Key aspects of debt consolidation include:

Improved cash flow due to lower monthly payments

Preserving credit score, as on-time payments are still made to creditors

Potential reduction in interest rates and overall debt repayment cost

Debt Settlement

Debt settlement involves negotiating with creditors to reduce the amount owed, often through a third-party debt settlement company. While it may result in a lower overall debt balance, it carries risks and potential negative consequences:

Fees charged by debt settlement companies

Potential negative impact on credit score due to late or missed payments

Possible tax implications, as forgiven debt may be considered taxable income

When considering debt consolidation or debt settlement, borrowers should carefully weigh the benefits and risks of each option and consult with a financial professional to determine the most appropriate strategy for their unique circumstances.

How Personal Loans Affect Your Credit

A personal loan can impact your credit in various ways, both positively and negatively:

Positive Impacts

Credit Mix: A personal loan adds to the diversity of your credit accounts, demonstrating your ability to manage different types of credit.

On-Time Payments: Making timely payments on your personal loan contributes to a positive payment history, which is a significant factor in your credit score.

Debt Consolidation: If used for debt consolidation, a personal loan can lower your credit utilization ratio by reducing credit card balances, which can positively impact your credit score.

Negative Impacts

Hard Inquiry: When you apply for a personal loan, a hard inquiry is recorded on your credit report, which can temporarily lower your credit score.

Increased Debt: Taking on additional debt through a personal loan may increase your debt-to-income ratio, which can negatively impact your creditworthiness.

Late Payments: Failing to make timely payments on your personal loan can damage your credit score and result in additional fees.

To ensure a personal loan has a positive impact on your credit, focus on making timely payments, managing your overall debt responsibly, and monitoring your credit report for accuracy.

Early Repayment of Personal Loans: Pros and Cons

Paying off a personal loan ahead of schedule can have both advantages and drawbacks:

Pros

Interest Savings: Early repayment can result in significant savings on interest costs.

Improved Credit Score: Reducing your overall debt can positively impact your credit score, especially if it lowers your credit utilization ratio.

Financial Freedom: Paying off a personal loan early can free up funds for other financial goals or expenses.

Cons

Prepayment Penalties: Some lenders may charge prepayment penalties for paying off a loan early, reducing potential savings.

Opportunity Cost: The funds used for early loan repayment might be allocated to other investments or financial goals with potentially higher returns.

When considering early repayment of a personal loan, weigh the potential benefits against the costs and evaluate your financial priorities to make an informed decision.

Go check out!!

- Investment Products: What Are Investment Products?

- Personal Loan: What Is Personal Loan?

- Savings Account: What Is Savings Account & How To Open It?

- Insurance Meaning: What Is It And Related Terms Explained

Personal Loan FAQs: Common Questions Answered

Can I get a personal loan with bad credit?

Yes, it is possible to obtain a personal loan with bad credit, but it may be more challenging to secure favorable loan terms.

Lenders may charge higher interest rates or require a co-signer to mitigate the risk associated with lending to a borrower with a poor credit history.

Sell as many financial apps as you want to earn your income online through this apps that enables you to gain knowledge of many other financial products.

Can I use a personal loan to start a business?

Yes, personal loans can be used to finance various aspects of starting a business, such as purchasing inventory, funding marketing efforts, or covering initial operating costs. However, it's essential to consider alternative financing options, such as business loans or grants, that may offer more favorable terms and tax benefits specifically designed for business expenses.

How long does it take to get a personal loan?

The time it takes to obtain a personal loan can vary depending on the lender and the borrower's individual circumstances. Some online lenders offer quick approval and funding within one to two business days, while traditional banks and credit unions may take longer to process and approve loan applications.

Are personal loans tax-deductible?

In most cases, the interest paid on personal loans is not tax-deductible. However, there are exceptions, such as when a personal loan is used for specific purposes like qualified education expenses or substantial home improvements. Consult a tax professional to determine if your personal loan interest is eligible for a tax deduction.

Can I have multiple personal loans at the same time?

It is possible to have multiple personal loans simultaneously, but it's essential to consider the potential impact on your credit score and overall financial health. Taking on additional debt can strain your budget, increase your debt-to-income ratio, and make it more challenging to manage multiple loan payments.

Personal Loan Checklist: Preparing for a Successful Application

Before applying for a personal loan, use this checklist to ensure you're well-prepared:

-

Review Your Credit Report: Ensure your credit report is accurate and dispute any errors that may negatively impact your credit score.

-

Determine Loan Purpose: Clearly define the purpose of the loan and how the funds will be used, as this can impact the loan type and terms.

-

Calculate Loan Amount: Assess your financial needs and determine a loan amount that is sufficient without overextending your budget.

-

Compare Lenders: Research and compare loan offers from multiple lenders to find the best interest rates, loan terms, and fees.

-

Gather Documentation: Collect necessary documents, such as proof of income, employment verification, and bank statements, to expedite the application process.

-

Create a Repayment Plan: Develop a repayment strategy that aligns with your budget and financial goals, considering factors such as the loan term, interest rate, and monthly payment.

By following this checklist, borrowers can better position themselves for a successful personal loan application and make informed decisions that support their financial objectives.

Personal Loan vs. Line of Credit: Which is Right for You?

When considering borrowing options, it's essential to understand the differences between personal loans and lines of credit to determine which best suits your needs:

Credit Cards Benefits

Convenience: Credit cards offer easy access to funds and may be a more convenient option for smaller or ongoing expenses.

Rewards and Perks: Some credit cards offer rewards, cash back, or other perks that can provide additional value.

Higher Interest Rates: Credit cards typically have higher interest rates than personal loans, making them a less cost-effective option for long-term borrowing.

Peer-to-Peer (P2P) Lending

Online Platforms: P2P lending platforms connect borrowers directly with individual investors, potentially offering more competitive interest rates and terms.

Flexible Loan Amounts: P2P loans can range from small to large amounts, providing borrowers with flexibility in meeting their financial needs.

Limited Regulation: P2P lending platforms may be subject to less regulation than traditional financial institutions, which could impact borrower protections and recourse options.

By evaluating these alternatives, borrowers can make informed decisions about the best borrowing option for their unique financial circumstances.

Personal Loans for Debt Consolidation: Advantages and Disadvantages

Using a personal loan for debt consolidation can offer both advantages and disadvantages:

Advantages

Simplified Payments: Combining multiple debts into a single loan streamlines monthly payments and simplifies debt management.

Lower Interest Rate: A personal loan may offer a lower interest rate than high-interest credit card debt, reducing overall interest costs.

Fixed Repayment Term: With a set repayment term, borrowers can establish a clear timeline for becoming debt-free.

Disadvantages

Potential Fees: Some personal loans may charge origination fees, which could offset potential interest savings.

Loss of Debt-Specific Benefits: Consolidating certain types of debt, such as federal student loans, may result in the loss of borrower benefits or protections specific to that debt.

Risk of Additional Debt: If borrowers continue to use credit cards or other revolving credit after consolidating, they may accumulate additional debt, negating the benefits of consolidation.

When considering using a personal loan for debt consolidation, carefully weigh the advantages and disadvantages to determine if it's the most appropriate solution for your financial situation.

Understanding Fixed and Variable Interest Rates on Personal Loans

Personal loans can have fixed or variable interest rates, each with unique

benefits and potential drawbacks:

Fixed Interest Rate

Predictable Payments: A fixed interest rate ensures the same monthly payment throughout the loan term, providing budget stability.

Unaffected by Market Conditions: Fixed rates do not change based on market interest rates, offering protection from potential rate increases.

Potentially Higher Initial Rate: Fixed rates may be higher initially than variable rates, resulting in higher costs if market rates remain stable or decrease.

Variable Interest Rate

Lower Initial Rate: Variable rates often start lower than fixed rates, potentially offering short-term savings.

Rate Fluctuations: Variable rates can change based on market conditions, resulting in fluctuating monthly payments and overall loan costs.

Interest Rate Caps: Some variable-rate loans have interest rate caps, which limit the maximum rate increase over the loan term.

When selecting a fixed or variable interest rate for a personal loan, consider factors such as your tolerance for payment fluctuations, the anticipated duration of the loan, and market interest rate trends.

This will help you choose the most suitable option for your financial needs and goals.

Personal Loans vs. Credit Card Cash Advances: Comparing Borrowing Options

When in need of immediate funds, borrowers might consider personal loans or credit card cash advances.

Each option has unique benefits and drawbacks:

Personal Loans

Lower Interest Rates: Personal loans typically offer lower interest rates than credit card cash advances, making them a more cost-effective option for borrowing.

Fixed Repayment Term: Personal loans have a set repayment term, providing a clear timeline for repayment and helping borrowers budget accordingly.

Application Process: Personal loans require an application and approval process, which can take longer than obtaining a cash advance.

Credit Card Cash Advances

Immediate Access to Funds: Credit card cash advances provide instant access to cash, making them convenient for emergency situations.

Higher Interest Rates: Cash advances often carry higher interest rates than personal loans, increasing the overall cost of borrowing.

Additional Fees: Cash advances may be subject to additional fees, such as ATM fees or cash advance fees charged by the credit card issuer.

When deciding between a personal loan and a credit card cash advance, consider factors such as the urgency of your financial need, the total cost of borrowing, and your ability to manage repayment.

KEY TAKEAWAYS

-

Personal loans are unsecured loans that can be used for a wide range of purposes, such as debt consolidation, home improvements, or emergencies.

-

These loans typically come with fixed interest rates and repayment terms, providing predictable monthly payments.

-

Credit scores, income, and debt-to-income ratios play a significant role in determining eligibility and interest rates for personal loans.

-

Shopping around and comparing offers from different lenders can help borrowers secure better loan terms and save on interest costs.

-

Responsible borrowing and timely repayments are essential to maintain a healthy credit score and avoid potential financial stress.