Term Life Insurance: What Is Term Life Insurance?

Learn about the benefits of term life insurance and how it can provide financial protection for your loved ones.

Understanding Term Life Insurance

Term life insurance is a type of life insurance policy that provides coverage for a specific period of time, typically 10, 15, 20, or 30 years. Unlike other types of life insurance policies, such as whole life insurance, term life insurance does not provide coverage for the policyholder's entire life. Instead, it provides coverage for a set period of time, during which the policyholder pays premiums to keep the policy in force.

How Term Life Insurance Works

When you purchase a term life insurance policy, you choose the coverage amount and the length of the term. You then pay premiums to the insurance company on a regular basis, typically monthly or annually, to keep the policy in force. If you die during the term of the policy, your beneficiaries receive a payout, also known as a death benefit, which is typically tax-free.

Benefits of Term Life Insurance

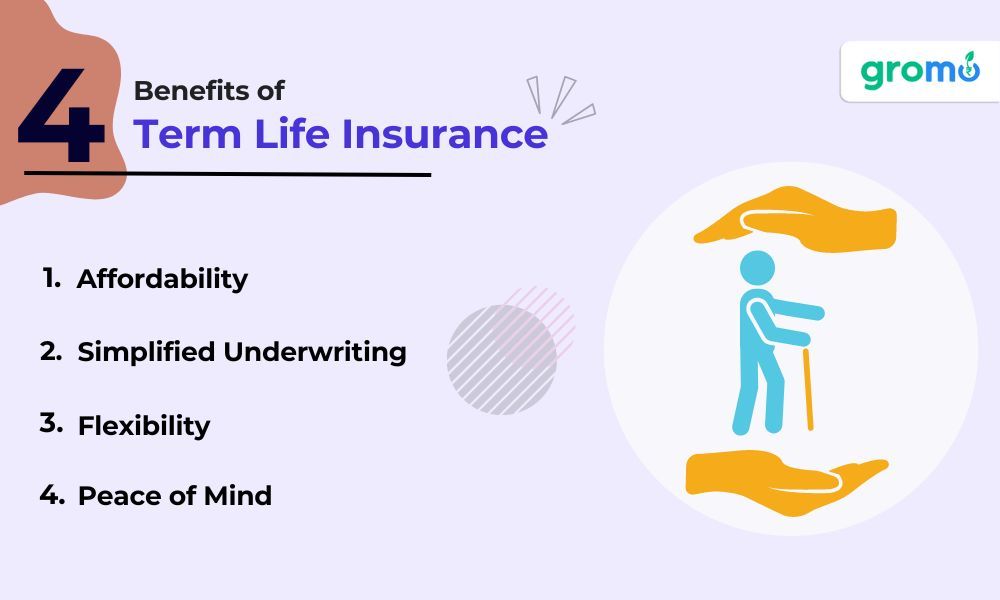

There are several benefits of term life insurance, including:

-

Affordability: Term life insurance is generally more affordable than other types of life insurance policies, such as whole life insurance.

-

Flexibility: Term life insurance policies can be customized to fit your specific needs and budget.

-

Simplified Underwriting: Term life insurance typically involves simpler underwriting than other types of life insurance policies, which means you may be able to get coverage without undergoing a medical exam.

-

Peace of Mind: Term life insurance provides peace of mind knowing that your loved ones will be financially protected if something happens to you.

Term Life Insurance vs. Other Types of Life Insurance

Term life insurance is just one of several types of life insurance policies. Other types of life insurance include whole life insurance, universal life insurance, and variable life insurance.

The main differences between term life insurance and these other types of life insurance are:

-

Coverage: Term life insurance provides coverage for a specific period of time, while other types of life insurance policies provide coverage for the policyholder's entire life.

-

Premiums: Term life insurance premiums are typically lower than premiums for other types of life insurance policies.

-

Cash Value: Term life insurance policies do not accumulate cash value, while other types of life insurance policies do.

Choosing the Best Term Life Insurance Policy for You

When choosing a term life insurance policy, there are several factors to consider, including:

-

Coverage Amount: The amount of coverage you need depends on your income, debts, and other financial obligations.

-

Term Length: The length of the term depends on your age, financial situation, and other factors.

-

Premiums: The premiums you pay will depend on your age, health, and other factors.

-

Insurance Company: It's important to choose a reputable insurance company with a strong financial rating.

Factors to Consider When Purchasing Term Life Insurance

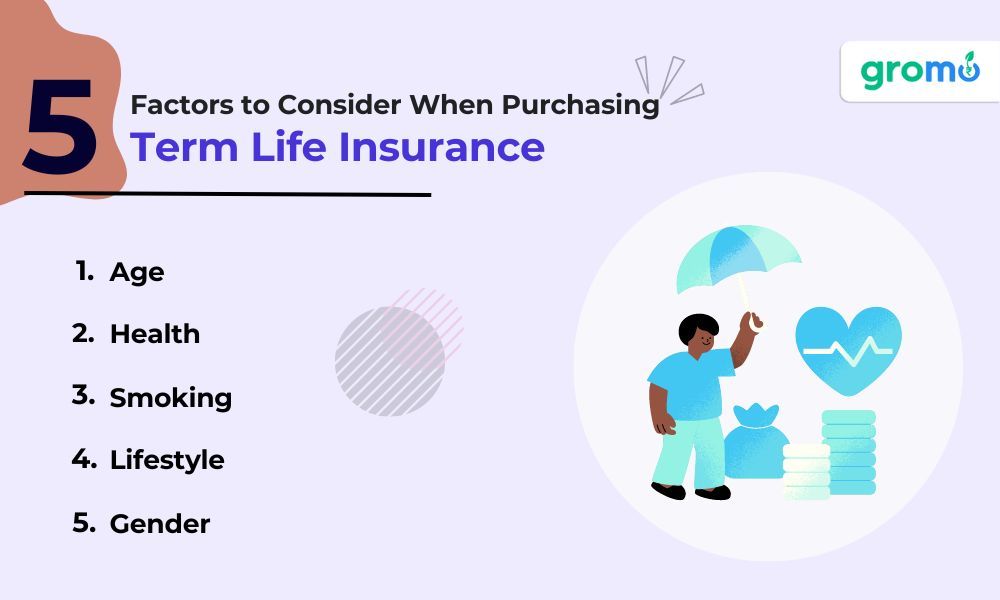

When purchasing term life insurance, there are several factors to consider, including:

-

Age: The younger you are when you purchase a policy, the lower your premiums will be.

-

Health: Your health will affect your premiums, and some health conditions may make it difficult to get coverage.

-

Smoking: Smokers typically pay higher premiums than non-smokers.

-

Lifestyle: Your occupation and hobbies may affect your premiums.

-

Gender: Women typically pay lower premiums than men because they have a longer life expectancy.

Term Life Insurance Calculator: How to Use It

A term life insurance calculator is a tool that helps you estimate how much coverage you need and how much it will cost. To use a term life insurance calculator, you will need to enter information such as your age, income, debts, and other financial obligations.

The calculator will then provide you with an estimate of how much coverage you need and how much it will cost.

Term Life Insurance Premiums and Tax Benefits

Term life insurance premiums are generally lower than premiums for other types of life insurance policies. In addition, term life insurance policies offer tax benefits. The premiums you pay for a term life insurance policy are typically tax-deductible, and the death benefit your beneficiaries receive is typically tax-free.

Top Term Life Insurance Providers in India

There are several top term life insurance providers in India, including:

Max Life Insurance

HDFC Life Insurance

LIC (Life Insurance Corporation) of India

SBI (State Bank of India) Life Insurance

Tata AIA Life Insurance

Policybazaar

When choosing a term life insurance provider, it's important to consider factors such as the company's financial rating, customer service, and reputation in the industry.

Before moving ahead, go check out-

- Things To Consider When Buying Motor Insurance In India

- Sell Insurance Policies & Earn Commission Online Without Any Investment

- 5 Best Credit Cards In India 2023

- 5 Best LIC Policies For Everyone In 2023

Final Thoughts: Why You Need Term Life Insurance

Term life insurance is an essential component of a comprehensive financial plan. It provides peace of mind knowing that your loved ones will be financially protected if something happens to you. Term life insurance is also affordable and flexible, making it a great choice for people who want to ensure their loved ones are protected without breaking the bank.

So far we understand, if you have financial obligations and dependents who rely on your income, term life insurance is a smart investment. It provides financial protection for your loved ones in the event of your unexpected death, and it's affordable and customizable to fit your specific needs and budget. When purchasing term life insurance, be sure to consider factors such as coverage amount, term length, premiums, and the reputation of the insurance provider.

Here are some additional tips to help you choose the best term life insurance policy for your needs:

-

Consider riders: Many providers offer riders, which are additional benefits that can be added to your policy for an additional cost. Some common riders include accidental death, disability waiver of premium, and child term rider. Consider adding riders that align with your needs and budget.

-

Compare quotes from multiple providers: To ensure that you're getting the best coverage for your needs and budget, it's important to compare quotes from multiple providers. Use a comparison tool or work with an independent agent to get quotes from multiple providers.

-

Read the fine print: Before choosing a policy, make sure to read the fine print and understand the terms and conditions of the policy. Look for any exclusions or limitations that may impact your coverage.

-

Choose the right beneficiary: When choosing a beneficiary for your policy, make sure to choose someone who will use the funds in a way that aligns with your wishes. Consider naming a secondary beneficiary in case your primary beneficiary is unable to receive the funds.

-

Keep your policy up-to-date: It's important to review your policy periodically and make any necessary updates to ensure that it still meets your needs. This includes updating your beneficiary, adjusting your coverage amount, and reviewing your policy features.

Now you can sell many other financial products using the GroMo app and earn more than you expect

DOWNLOAD GROMO APP

When comparing term life insurance policies, it's important to look for policies that provide the right amount of coverage for your needs. You should consider the amount of debt you have, the number of dependents you have, and your future financial obligations. You should also consider the length of the term, which is typically 10, 15, 20, or 30 years.

Return of premium term life insurance is another option to consider. With this type of policy, if you outlive the term of the policy, you will receive a refund of the premiums you paid. However, these policies are typically more expensive than traditional term life insurance policies.

Another option to consider is group term life insurance, which is often provided by employers. These policies provide coverage for employees at a lower cost than individual policies. However, group term life insurance policies typically have lower coverage limits than individual policies, and the coverage ends when you leave the employer.

Term life insurance is an essential component of a comprehensive financial plan. It provides financial protection for your loved ones in the event of your unexpected death, and it's affordable and customizable to fit your specific needs and budget. When purchasing term life insurance, be sure to consider factors such as coverage amount, term length, premiums, and the reputation of the insurance provider.

In addition, it's important to review your term life insurance policy periodically to ensure that it still meets your needs. If your financial situation changes, you may need to adjust the coverage amount or term length. For example, if you have a child, buy a house, or start a business, you may need to increase your coverage amount.

Finally, it's important to choose a reputable and financially stable insurance provider. Look for providers that have high financial ratings and good customer service ratings. You can also check with your state's insurance department to see if any complaints have been filed against the provider.

Overall, term life insurance is a valuable investment that provides financial protection for your loved ones. By choosing the right coverage amount and term length, you can ensure that your loved ones are protected in the event of your unexpected death.

Before moving forward download the GroMo app where you can sell term life insurance and many other financial products and earn as much as you want.

Here are the key benefits and considerations of term life insurance:

Affordable

Term life insurance is typically the most affordable type of life insurance, making it accessible for many people.

Customizable

Term life insurance policies can be tailored to fit your specific needs, with coverage amounts and term lengths that can be adjusted based on your financial situation.

No cash value

Unlike some other types of life insurance policies, term life insurance does not accumulate cash value over time.

Coverage ends

Once the term of the policy is over, the coverage ends. If you still need coverage, you will need to purchase a new policy.

No equity

Because term life insurance does not accumulate cash value, there is no equity that you can borrow against.

Flexibility

Term life insurance policies can be converted to permanent life insurance policies if your needs change over time.

No dividend payments

Unlike some types of permanent life insurance, term life insurance policies do not pay dividends.

When choosing a term life insurance policy, it's important to consider your specific needs and financial situation. Work with a trusted insurance agent to compare policies from different providers and find the best coverage for your needs. With the right term life insurance policy in place, you can have peace of mind knowing that your loved ones will be taken care of in the event of your unexpected death.

When shopping for term life insurance, it's important to compare policies from different providers to find the best coverage for your needs.

Here are some factors to consider when comparing term life insurance policies:

Coverage amount: Determine how much coverage you need based on your financial obligations and future needs. Consider factors such as your debts, mortgage, and the needs of your dependents.

Term length: Choose a term length that aligns with your financial obligations and goals. Shorter terms are typically less expensive, but may not provide sufficient coverage if you have long-term financial obligations.

Premiums: Consider the cost of premiums for the coverage amount and term length you need. Compare premiums from different providers to find the best value.

Financial strength: Choose a provider that is financially stable and has a strong reputation in the industry. Check the provider's financial ratings and customer service ratings.

Policy features: Look for policies that offer features that align with your needs, such as guaranteed renewability, conversion options, and accelerated death benefits.

Underwriting process: Consider the underwriting process and how it may impact your premiums and coverage. Some providers offer simplified underwriting that can result in faster approval and lower premiums.

By considering these factors, you can find the best term life insurance policy for your needs and budget. It's important to review your policy periodically to ensure that it still meets your needs and to make any necessary adjustments. With the right term life insurance policy in place, you can have peace of mind knowing that your loved ones will be protected in the event of your unexpected death.

Finally, it's important to review your policy periodically to ensure that it still meets your needs. As your financial situation and family obligations change over time, your life insurance needs may also change. Review your policy regularly and make any necessary adjustments to ensure that your loved ones will be protected in the event of your unexpected death.

GO CHECK OUT-

- Insurance Meaning: What Is It And Related Terms Explained

- How To Get The Best Credit Cards In India?

- Things To Consider When Buying Motor Insurance In India

- Consequences Of Having A Low CIBIL Score

KEY TAKEWAYS

-

Term life insurance is a type of life insurance that provides coverage for a specified period, typically 10, 20, or 30 years.

-

The premiums for term life insurance are generally lower than those for permanent life insurance, making it an affordable option for those on a budget.

-

Term life insurance is an excellent choice for young families, as it can provide financial protection for dependents in case of the policyholder's unexpected death.

-

When choosing a term life insurance policy, it's important to consider the length of the term, the amount of coverage needed, and any riders or additional benefits that may be available.

-

It's crucial to shop around and compare quotes from multiple insurers to get the best possible coverage at an affordable price. Additionally, it's recommended to review and update the policy regularly to ensure it meets changing needs over time.